Home > Investor Relations > Financials and Materials > Annual Report > Message from the CFO

Message from the CFO

Makoto Shinmura

Senior Managing Executive Officer

Charting a course toward higher corporate value by maximizing returns for all stakeholders

Embarking on the new Medium-term Management Plan (FY2026 through FY2028)

It has been one year since I wrote in last year’s Integrated Report that we would continue to communicate the directions indicated by our compass and the specific path forward through our disclosures and investor relations activities.

We have now embarked on the new Medium-term Management Plan. Covering the period from fiscal 2026 through fiscal 2028, this plan marks a major turning point for the Bank.

Under the new Medium-term Management Plan, we established our Medium- to Long-term Vision, which defines where we aspire to be 15 years from now, based on a back casting approach rooted in our Purpose and Management Philosophy while taking into account changes in the internal and external environment surrounding the Bank.

This vision comprises two aims. The first is to become Japan’s leading comprehensive financial platform, providing financial products and services anytime and anywhere across Japan through both physical and digital channels in response to the increasingly diverse needs of our customers.

The second is to become a leading global market player, achieving an optimal portfolio and earnings profile while also developing an asset management business, supported by approximately 180 trillion yen in deposits entrusted to us by roughly 120 million customers through our nationwide post office and branch network.

Together, these two aims represent the destination indicated by our compass.

We will move forward with all officers and employees united as one, working together toward the achievement of these visions.

For further details on the new Medium-term Management Plan, please also refer to page 28.

Looking back on fiscal 2025: the departure point for the new Medium-term Management Plan

During fiscal 2025, the global economy remained primarily resilient, led by the United States, even as uncertainty stemming from U.S. tariff policies persisted. In Japan, the economy continued its gradual recovery, supported in part by a rebound in domestic demand, leading the Bank of Japan to raise its policy interest rate in December 2025.

Meanwhile, the escalation of tensions in the Middle East since February 2026 has made the outlook for the macroeconomic environment even more difficult to predict. While changes such as the domestic interest rate environment have created tailwinds for financial institutions, they have also heightened the importance of risk management – specifically being prepared for shifting waves of geopolitical and other risks.

Going forward, we will continue to steer the Bank with care as we navigate an ever-changing business environment.

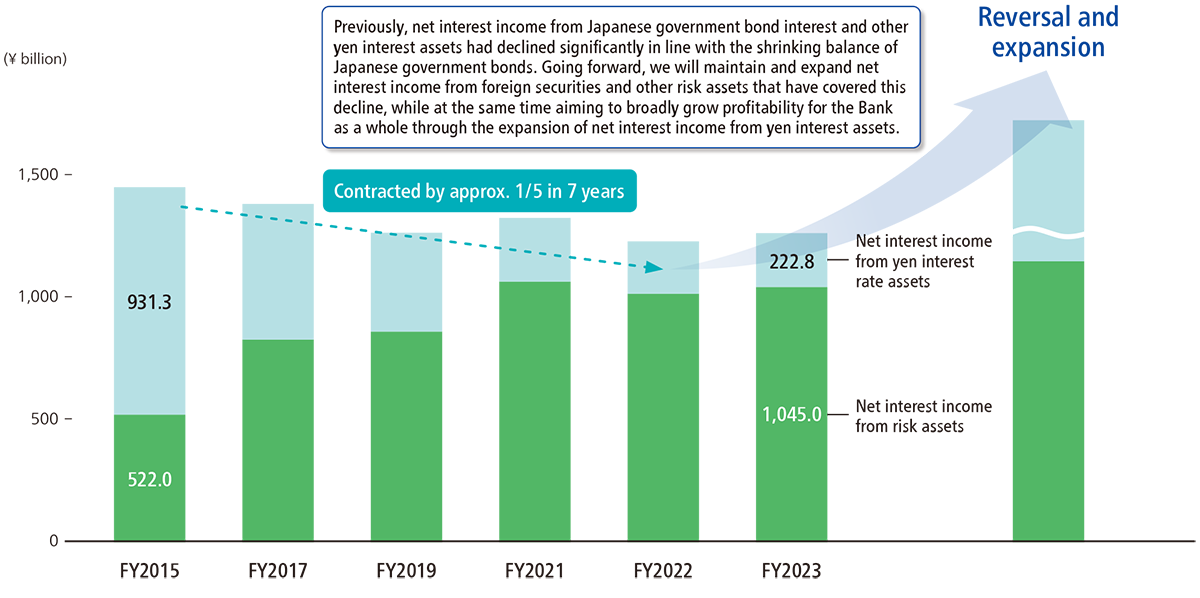

In response to rising domestic interest rates, the Bank steadily shifted assets from deposits with other institutions into Japanese Government Bonds, while continuing to invest in risk assets with appropriate risk controls in place and in line with changing market conditions.

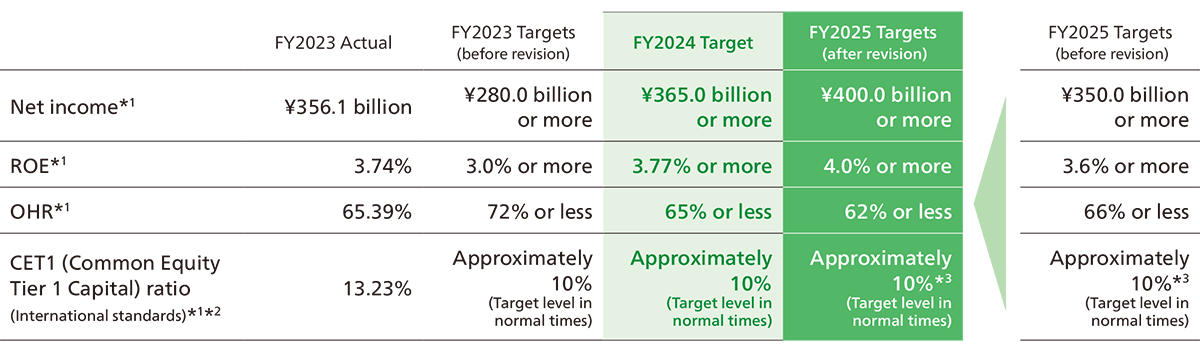

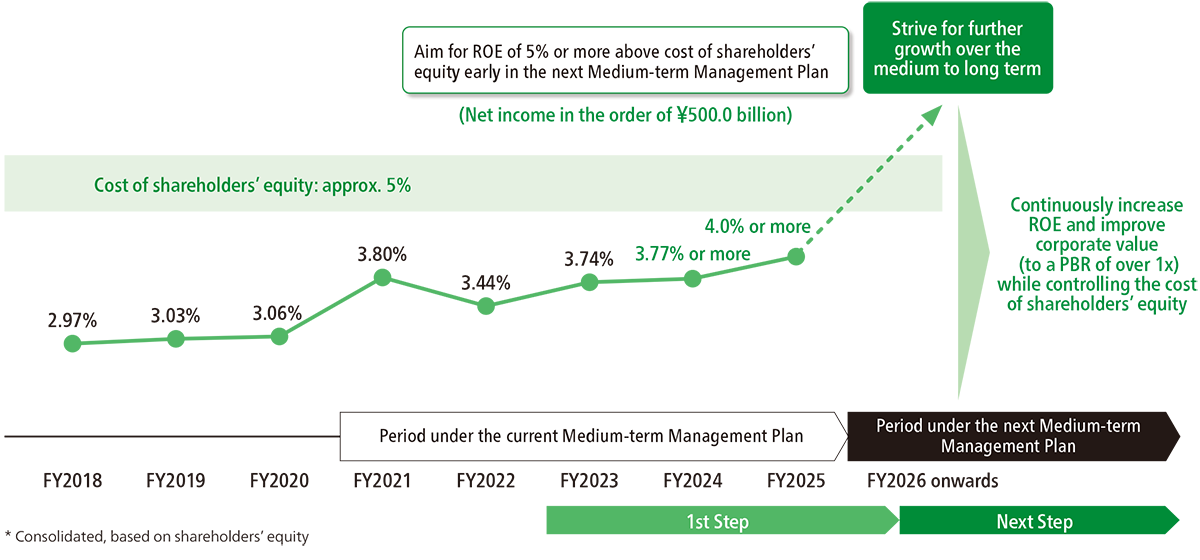

As a result, net income reached 525.5 billion yen, marking a record high for the third consecutive year since our listing.

The dividend per share amount has increased steadily, rising from 51 yen in fiscal 2023 to 58 yen in fiscal 2024 and reaching a record-high 74 yen in fiscal 2025.

In addition, from December 2025 through March 2026, we conducted share buybacks aimed at enhancing shareholder returns and improving capital efficiency.

I believe our ability to achieve steady earnings growth while strengthening shareholder returns accordingly provided a solid foundation as we embarked on the new Medium-term Management Plan.

Sustainable enhancement of corporate value at the heart of management

As CFO, responsible for financial and capital strategy, I am expected to serve as a navigator, supporting the Bank’s growth through appropriate financial strategies and helping to enhance sustainably corporate value amid a changing business environment.

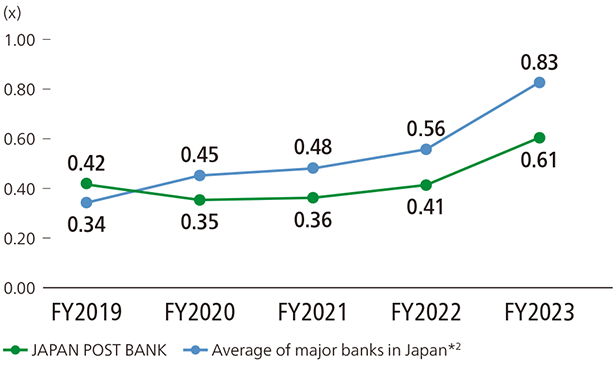

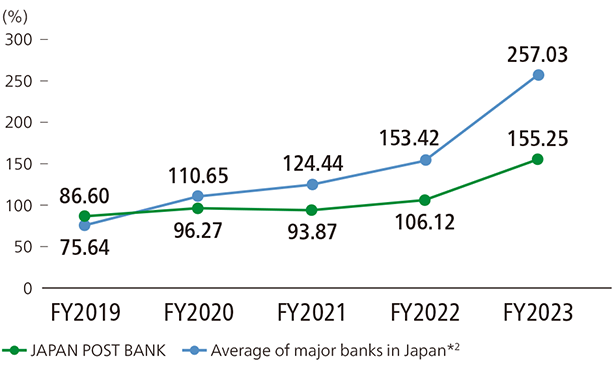

In fiscal 2025, we achieved profit growth for the third consecutive year, and our price-to-book (P/B) ratio temporarily rose above 1.0x. However, we continue to lag behind Japan’s major banking groups.

I recognize that enhancing corporate value remains a work in progress and continues to be a significant management challenge.

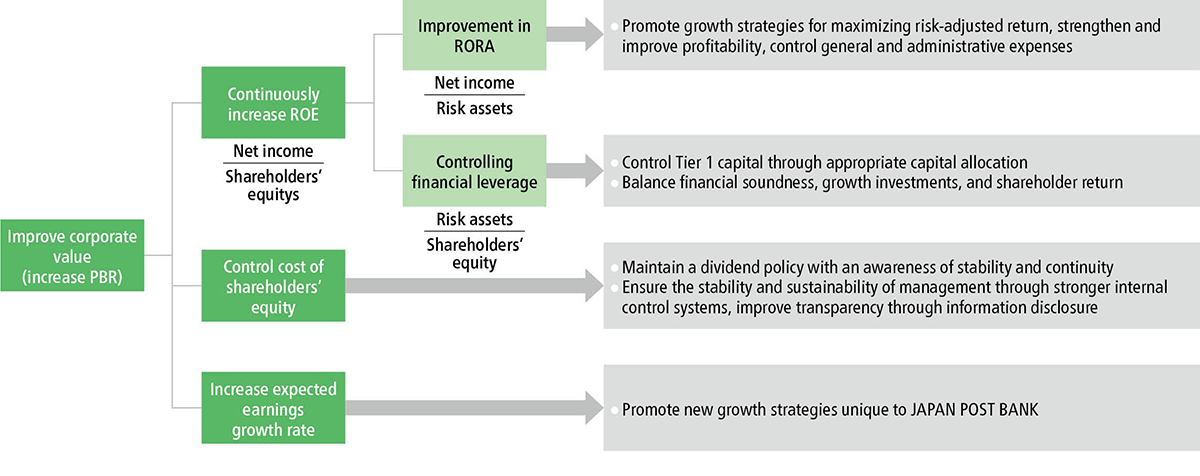

We analyze our price-to-book (P/B) ratio by breaking it down into return on equity (ROE) and the price-to-earnings ratio (PER). As shown in Figure 3, we believe it is necessary to first raise our ROE, which currently lags behind those of Japan’s major banking groups.

The new Medium-term Management Plan is also a plan to significantly enhance corporate value by pursuing the realization of our Medium- to Long-term Vision.

As shown in Figure 5, the four business strategies presented in the new Medium-term Management Plan, together with the initiatives to strengthen the management foundation that support them, will contribute directly to improving ROE and increasing PER.

I believe that when every officer and employee fulfills the role expected of them at every level of the organization, it will not only enhance corporate value but also create a positive impact on society, ultimately benefiting all stakeholders, including shareholders and employees.

Sustainably improving ROE: Achieving our ambitious earnings targets

Under the new Medium-term Management Plan, we have set targets of approximately 10% ROE and net income of more than 1 trillion yen by fiscal 2028, representing a non-linear earnings growth trajectory that significantly exceeds our historical growth trend.

These earnings targets were established based on the environment surrounding the Bank and the challenges we face. They are not easily attainable low hurdles but rather targets that all officers and employees must work together to achieve.

Steady execution of our business strategies

The key to achieving these ambitious targets lies in the steady execution of the four business strategies set forth in the new Medium-term Management Plan.

Through our nationwide network of post offices and branches, we hold approximately 180 trillion yen in deposits entrusted to us by approximately 120 million accounts, primarily held by individual customers. As such, our first priority is to further strengthen this customer base.

Under the Digital Payment Business Strategy, we will strategically leverage the Yucho Bankbook App, which is used by more than 16 million customers, to offer services that are not only safe, secure, and convenient, but also provide beneficial services to customers.

Under the Consulting Business Strategy, we will expand our range of products and services, including through partnerships with external companies, and deliver services through an integrated mix of physical, remote, and digital channels.

Through these initiatives, we aim to become the financial institution of choice for our customers, while expanding Net fees and commissions and strengthening our customer base.

The Market Operation and Asset Management Business Strategy is designed to maximize the Bank’s earnings through the management of funds entrusted to us by our customers.

Benefiting from rising domestic interest rates, earnings from yen interest rate assets, including Japanese Government Bonds, are increasing at an accelerated pace. At the same time, we will continue to invest in risk assets with a focus on risk/return, utilizing indicators such as return on risk-weighted assets (RORA).

In April 2026, we established JP Asset Management Co., Ltd. to leverage the investment expertise we have cultivated over the years and take on the challenge of developing an asset management business. By combining the respective strengths of JP Asset Management Co., Ltd., which has supported asset building for individual customers, and Japan Post Investment Corporation, which has developed a business serving institutional investors primarily through private equity fund investments, we will respond to growing momentum toward establishing Japan as a leading asset management center.

Under the Regional and Corporate Solutions Business Strategy, we will further expand our domestic private equity investment activities, centered on Japan Post Bank Capital Partners Co., Ltd., while strengthening our corporate customer base through collaboration with regional financial institutions and the enhancement of services for corporate clients.

We believe the steady execution of these four business strategies will serve as the driving force behind improving the “R” in ROE.

Cost control

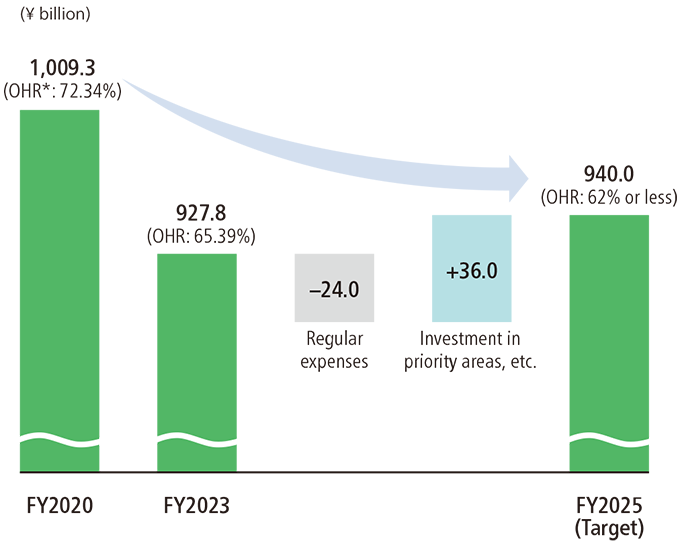

In addition to improving earnings power through the execution of our business strategies, disciplined cost control is essential to improving ROE.

We will continue to invest in cybersecurity and AML/CFT/CPF,* which are critical areas underpinning the Bank’s credibility, while also making proactive strategic investments in productivity-enhancing initiatives, including AI.

We will also continue to invest in human capital, including improving employee compensation and benefits.

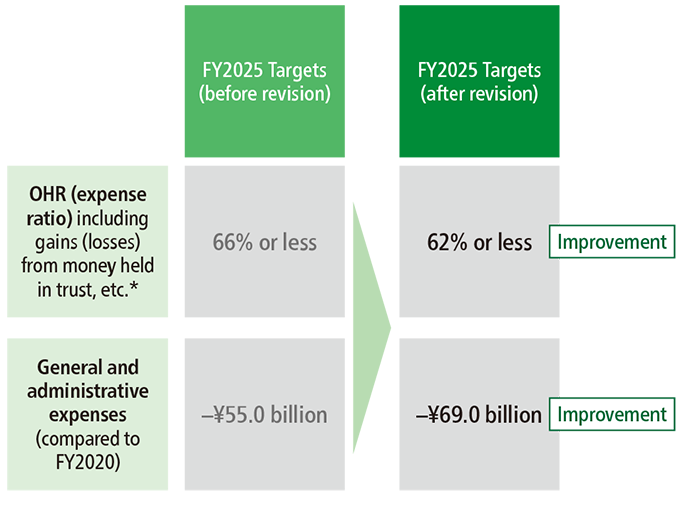

Throughout the period covered by the new Medium-term Management Plan, we will limit the overall increase in expenses to approximately the rate of inflation (around 3% per year). By balancing efficiency and growth, we aim to achieve an overhead ratio (OHR) of approximately 40%.

- * Anti-money laundering, countering terrorist financing, and countering proliferation financing.

Capital control

Capital policy was one of the key themes discussed most intensively and carefully during the formulation of the new Medium-term Management Plan.

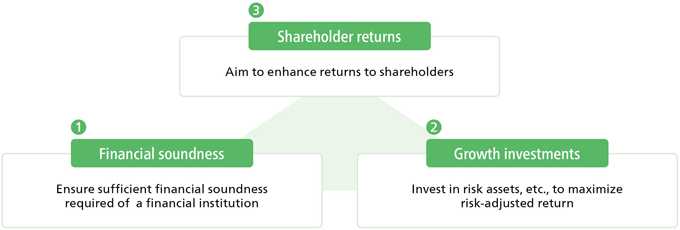

As shown in Figure 8, the Bank’s capital policy is based on maximizing a cycle of maintaining financial soundness, achieving earnings growth through growth investments, and returning value to shareholders.

In addition, we aspire to be the most familiar and trusted bank throughout Japan. To ensure that we do not undermine that trust, we have traditionally maintained a minimum required capital level.

Under the new Medium-term Management Plan, however, in light of continued capital accumulation, we have revised our approach and established a target capital range based on the characteristics of the Bank’s portfolio and various simulations.

Going forward, we will continue to pursue the optimal balance among shareholder returns, financial soundness, and growth investments while closely monitoring market conditions, and will strive to maintain appropriate capital management.

(1) Further enhancement of shareholder returns

Shareholder returns are one of the most important themes of our capital policy. During the period covered by the new Medium-term Management Plan, we intend to maintain a dividend payout ratio of approximately 50% and implement progressive dividends in line with earnings growth.

For fiscal 2026, we plan to increase the annual dividend per share by 19 yen, to 93 yen, and will continue to expand dividends in line with earnings growth.

In addition, in fiscal 2025, the final year of the previous Medium-term Management Plan, we conducted share buybacks with the aim of strengthening shareholder returns and improving capital efficiency, reflecting the fact that we achieved earnings exceeding our target level.

We will continue to consider share buybacks for fiscal year 2026 and beyond, taking into account market conditions, growth investment opportunities, and the Japan Post Group’s policy regarding its shareholding in the Bank.

Looking ahead, if earnings grow at a pace exceeding our targets, we would like to consider providing additional returns to shareholders in some form, taking into account our capital position.

(2) Ensuring financial soundness

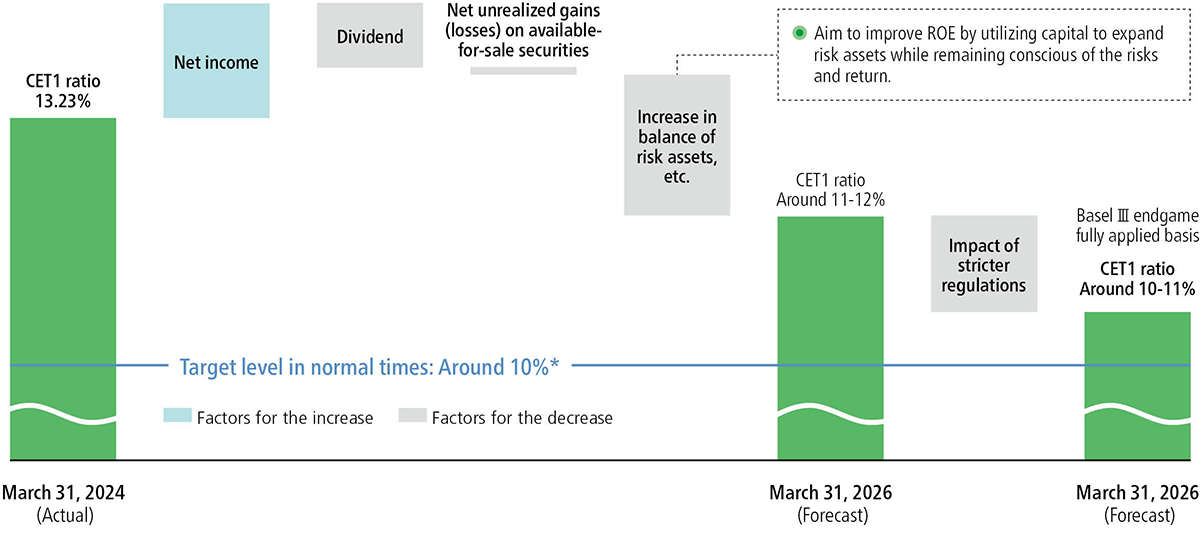

Although the Bank is subject to Japan’s domestic capital adequacy standards, we have managed our capital internally using the Common Equity Tier 1 (CET1) ratio under the international standards, reflecting factors such as the size of our overseas credit exposure.

Under the previous Medium-term Management Plan, our target level in normal times was approximately 10%. However, based on extensive simulations that took into account factors such as the characteristics of our portfolio, including the high proportion of securities investments within our investment portfolio, we have revised our target range to approximately 11%–13%.

Our basic response policy for each capital level is shown in Figure 9.

Going forward, we will continue to closely monitor market conditions and manage capital within this target range, while maintaining a strong focus on financial soundness.

(3) Growth investments

To improve ROE and sustain the Bank’s medium- to long-term growth, we will pursue growth investments more proactively and strategically than ever before.

At the same time, we will continue to steadily advance market investments that contribute to improving risk/return indicators, including RORA.

At present, a significant portion of the Bank’s earnings is generated through market operations. Accordingly, through strategic growth investments, we aim to strengthen earnings capacity in areas such as the retail and asset management businesses and build a more resilient earnings base that is less susceptible to fluctuations in market conditions.

Improving PER (expected earnings growth rate): Reducing the cost of shareholders’ equity and achieving sustainable growth

Reducing the cost of shareholders’ equity

Under the new Medium-term Management Plan, we have also deepened our discussion of how we assess the cost of shareholders’ equity. Based on calculations using multiple methodologies, we recognize that the Bank’s cost of shareholders’ equity is in the range of 6%–8%.

However, these figures are merely reference values derived from quantitative models. Through ongoing dialogue with investors, we intend to refine our assessment while taking market views into account.

To reduce the cost of shareholders’ equity, it is important to lower earnings volatility and achieve stable earnings growth. We also recognize that it is essential to respond appropriately and in a timely manner to a range of business risks, including cybersecurity risks.

We will continue to engage in dialogue with investors and strive to achieve highly transparent management that minimizes the risk of negative surprises.

Enhancing expected earnings growth

The Bank is both a financial institution with one of the largest retail networks in Japan and one of the world’s leading institutional investors. By leveraging these strengths and steadily executing our four business strategies, we will work to achieve earnings growth and enhance corporate value.

In addition, as we strive to become the most familiar and trusted bank, we aim to contribute to addressing social challenges by ensuring stable access to financial platforms, helping to realize a sustainable environment and society, and supporting the development of vibrant regional communities.

Supported by rising domestic interest rates, the Bank’s share price reached a post-listing record high in 2026. However, the banking industry is generally susceptible to changes in market conditions.

By steadily executing the various strategies set out in the new Medium-term Management Plan, we aim to build the Bank’s own enduring trust and value that are less dependent on the external environment.

To all our stakeholders, including shareholders and investors

When we announced the outline of our new Medium-term Management Plan in November 2025, we received extensive feedback, support, and encouragement from our stakeholders. I would like to once again express my sincere appreciation for your interest in the Bank’s new strategy and for each of the comments you shared, which were both candid and constructive.

Approximately six months have passed since we announced the outline of the plan. During that time, we have carefully considered the feedback we received and engaged in extensive discussions within the Bank, culminating in the formal announcement of the plan in May of this year.

Going forward, we will steadily execute the new Medium-term Management Plan and continue our journey toward realizing our vision.

We will continue to listen carefully to your feedback through our investor relations activities and other opportunities, and reflect it appropriately in our management, thereby enhancing corporate value on a sustainable basis.

We sincerely appreciate your continued understanding and support.